First Class Info About Closing Entries For Retained Earnings Opinion On Financial Statements

Solved Post The Closing Entries Of Retained Earnings To Note Payable Cash Flow Statement Financial Comparison Analysis

[solved] Describe The Yearend Closing Process. What Are Four Steps Managing Cash Flow Examples Profit And Loss For Dummies

Chapter 3 Add Depreciation, Closing Entries, 4 Diff Timelines Accts, Objectives Of Accounting For Income Taxes Prepaid Expenses Financial Statement

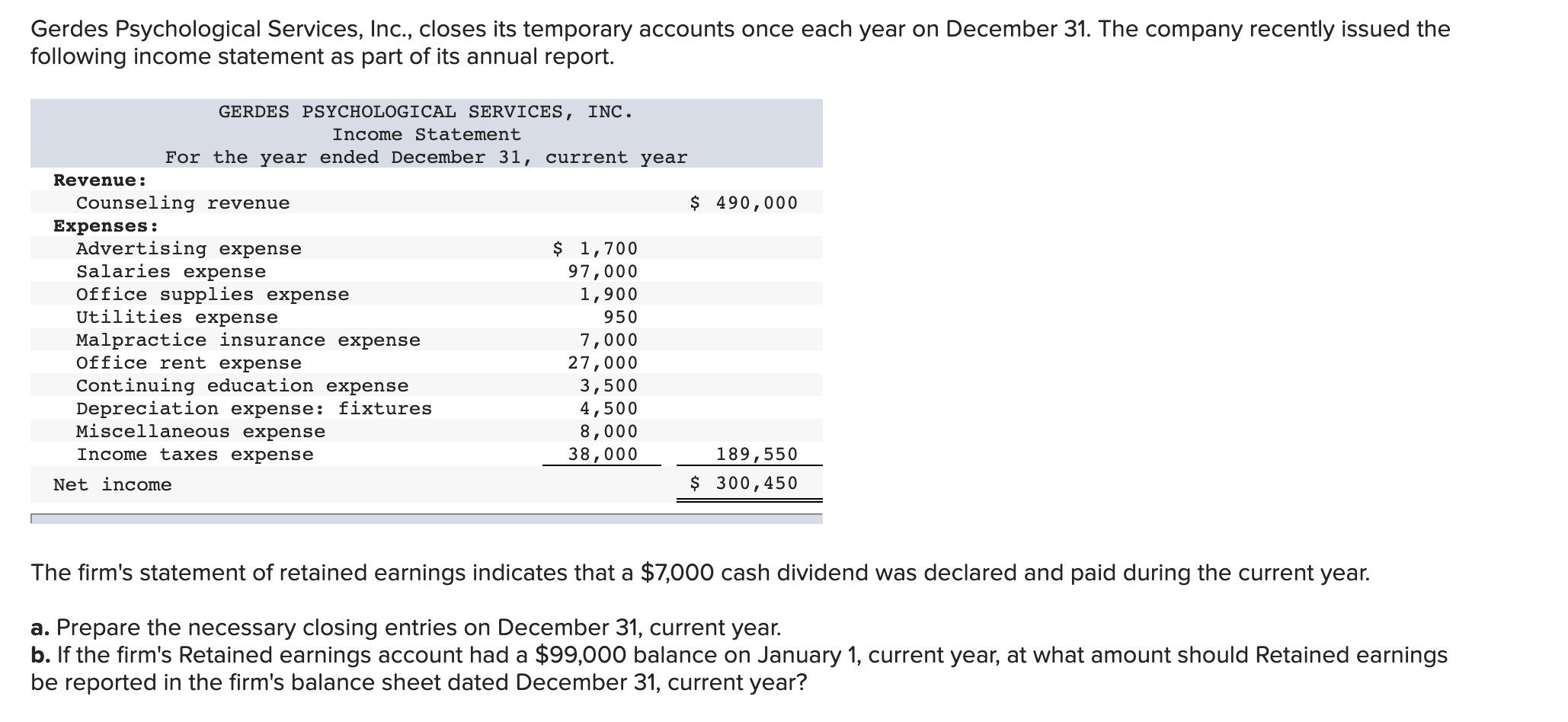

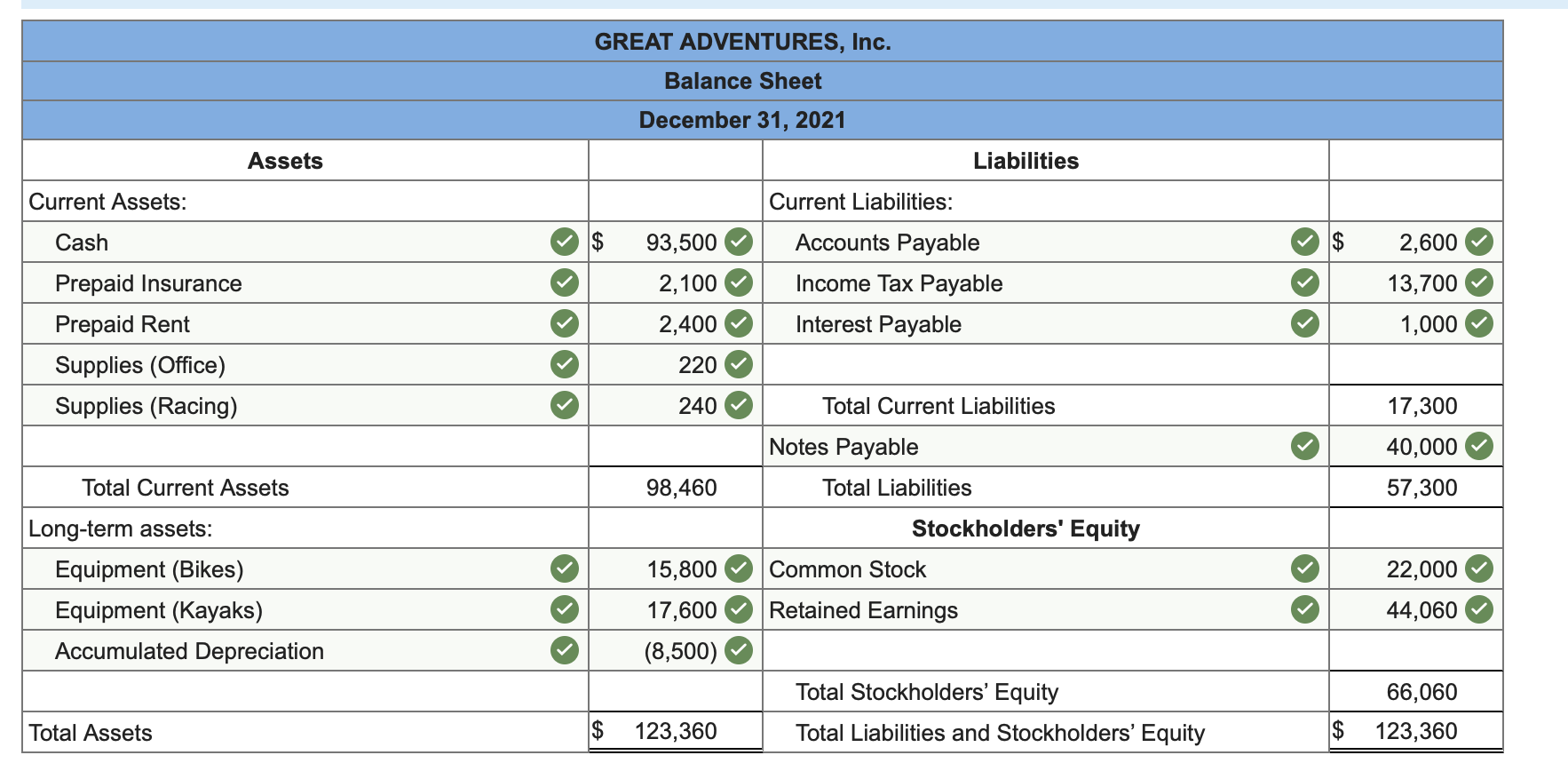

Solved A. Prepare The Necessary Closing Entries On December Explanatory Notes Financial Statements Statement Of Cash Flows Shows

Lo 5.1 Describe And Prepare Closing Entries For A Business Spscc Deferred Revenue Statement Of Cash Flows Profit Loss Chart Accounts

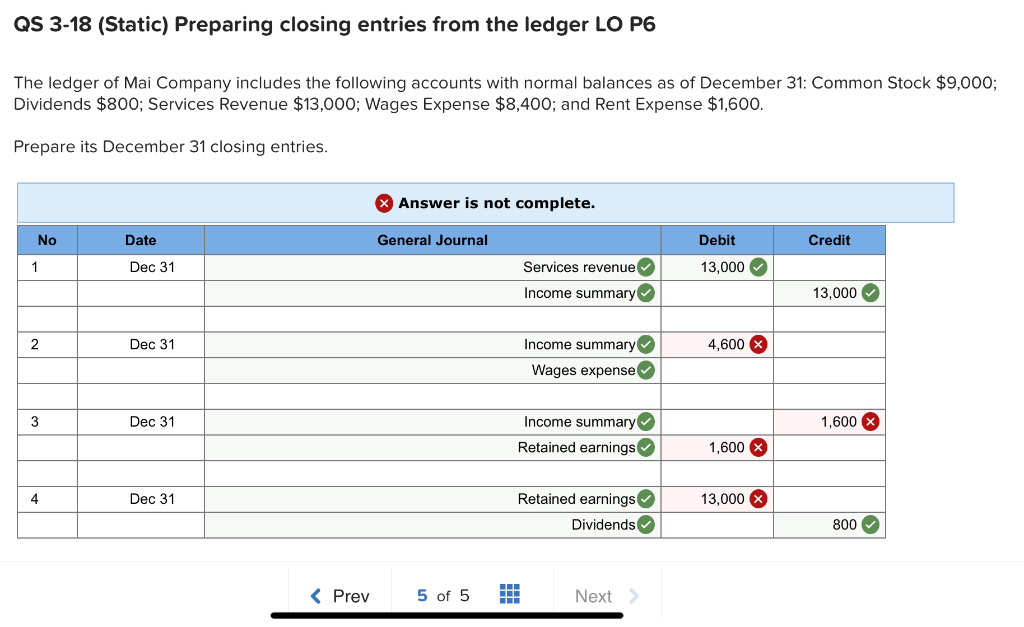

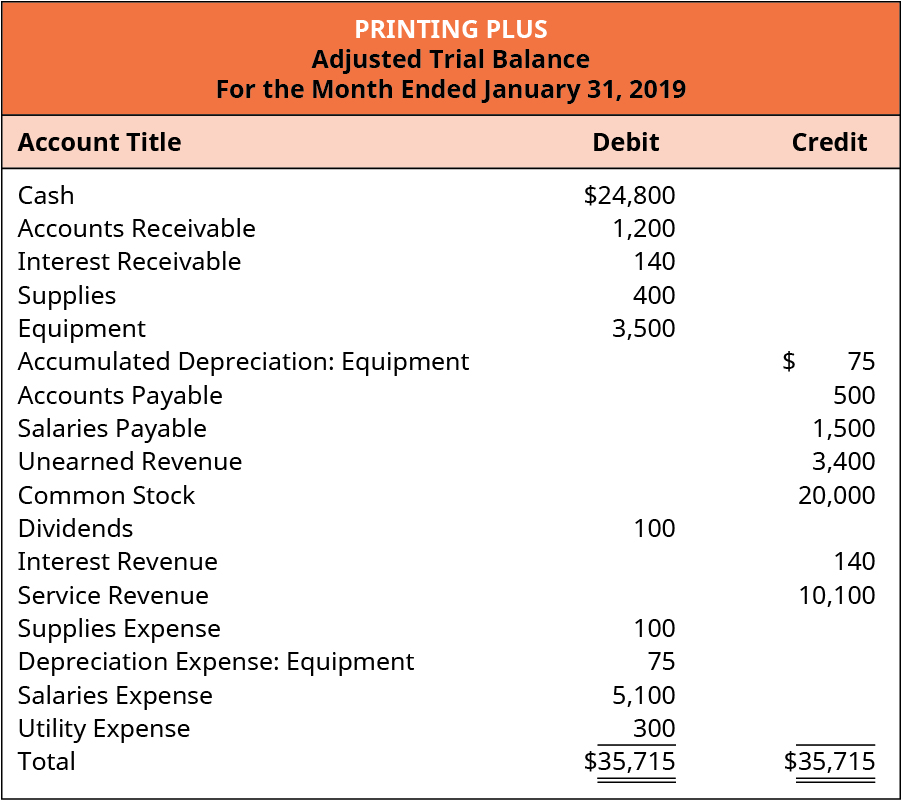

Solved Qs 318 (static) Preparing Closing Entries From The Bhel Financial Statements Income Statement Example Accounting

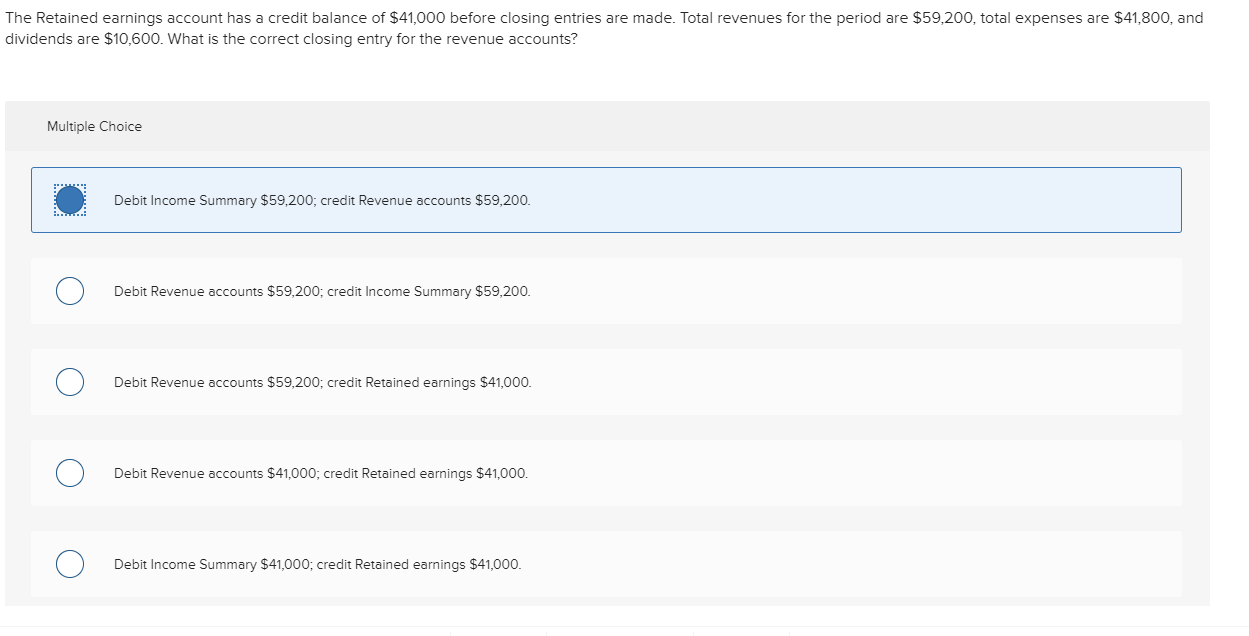

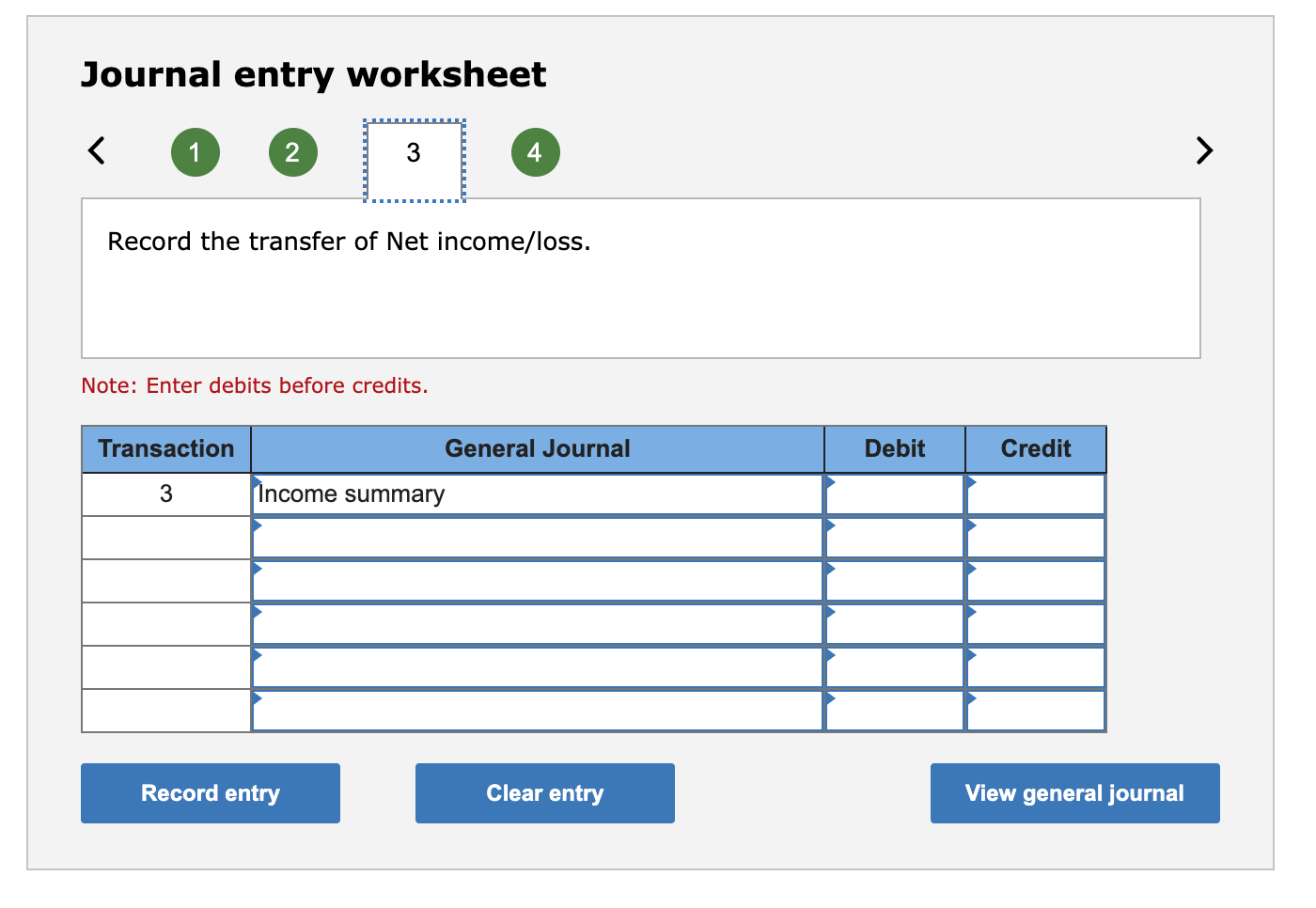

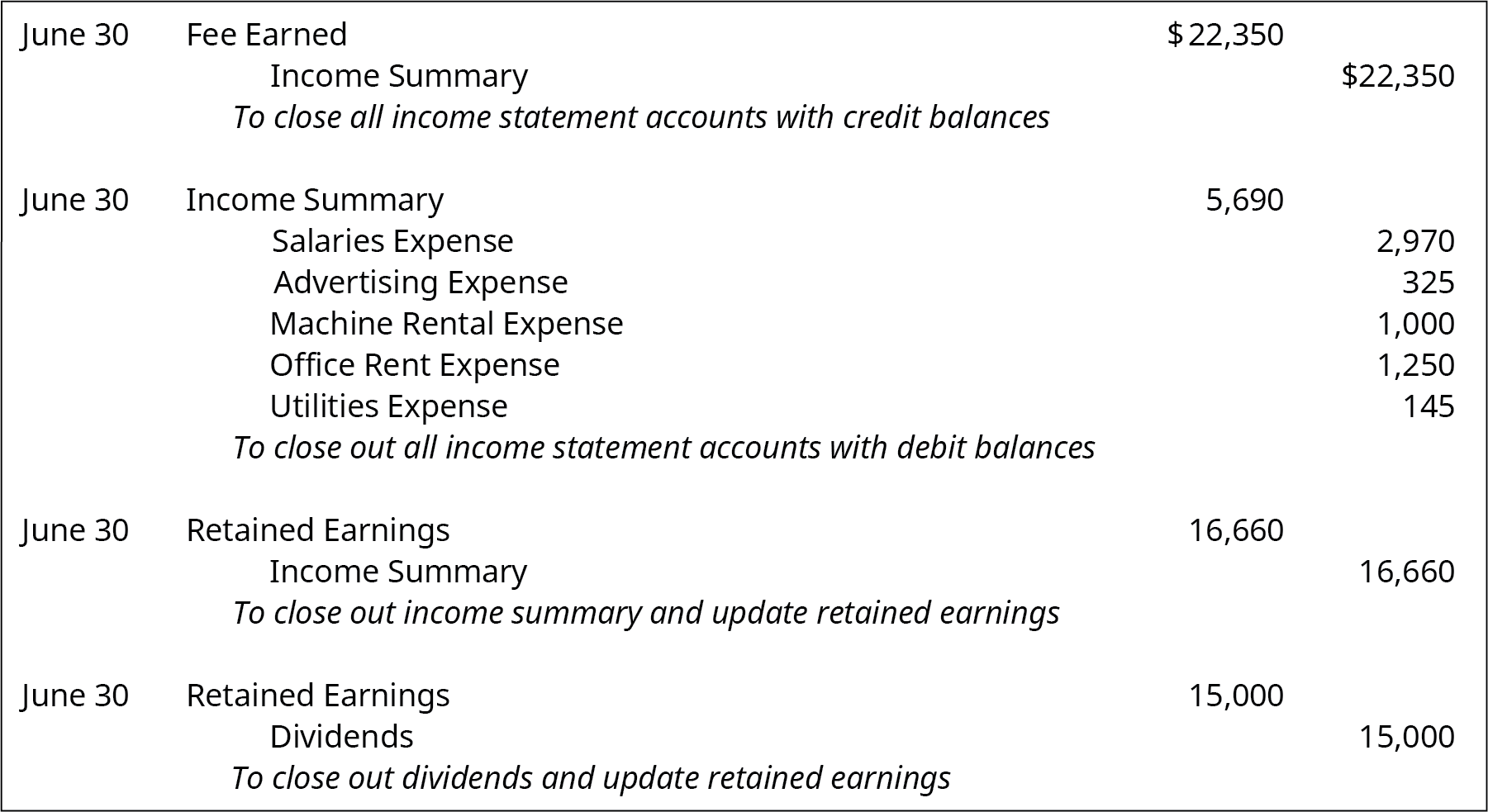

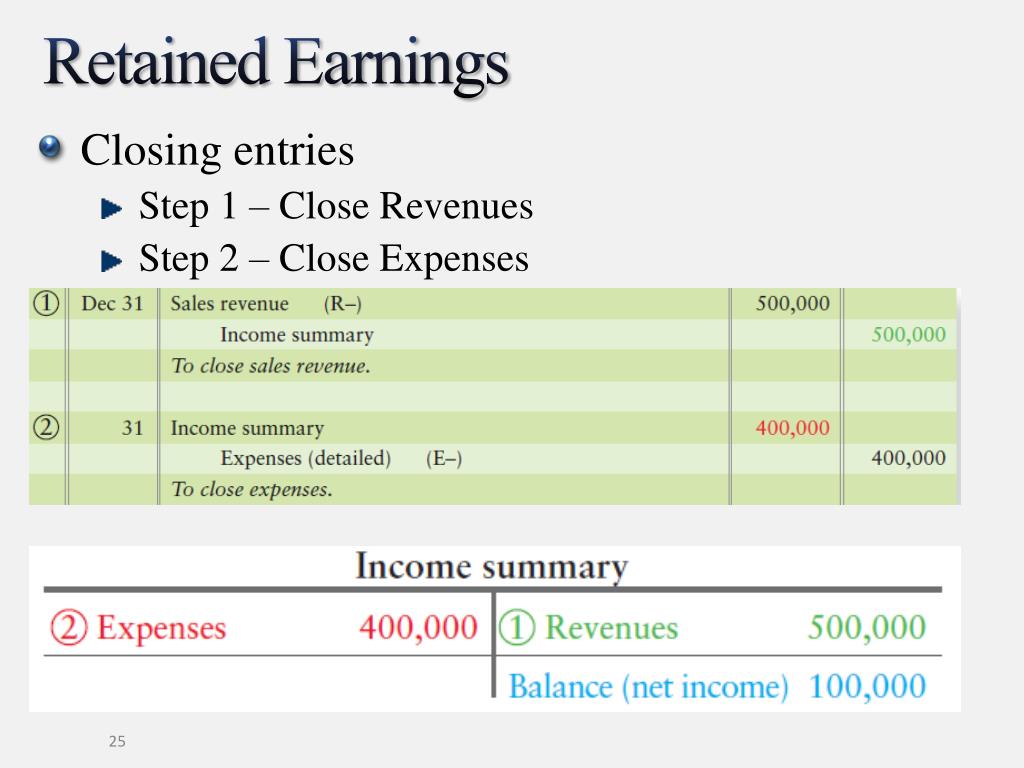

Now that we have closed income and expenses, we need to move the balances from the income summary to retained.

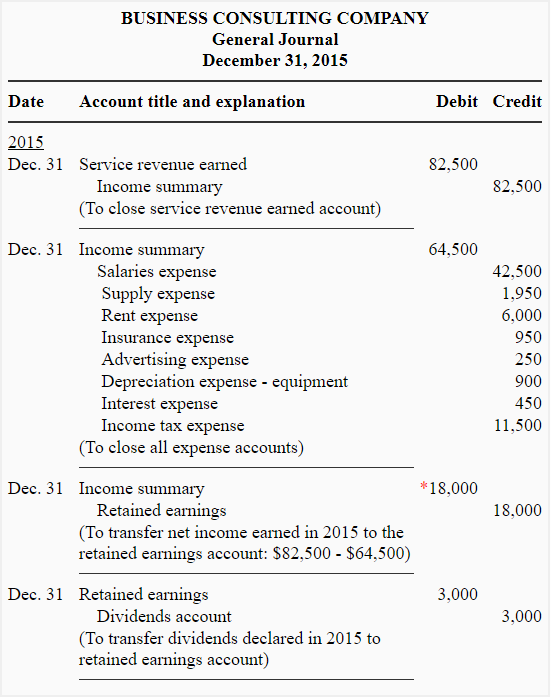

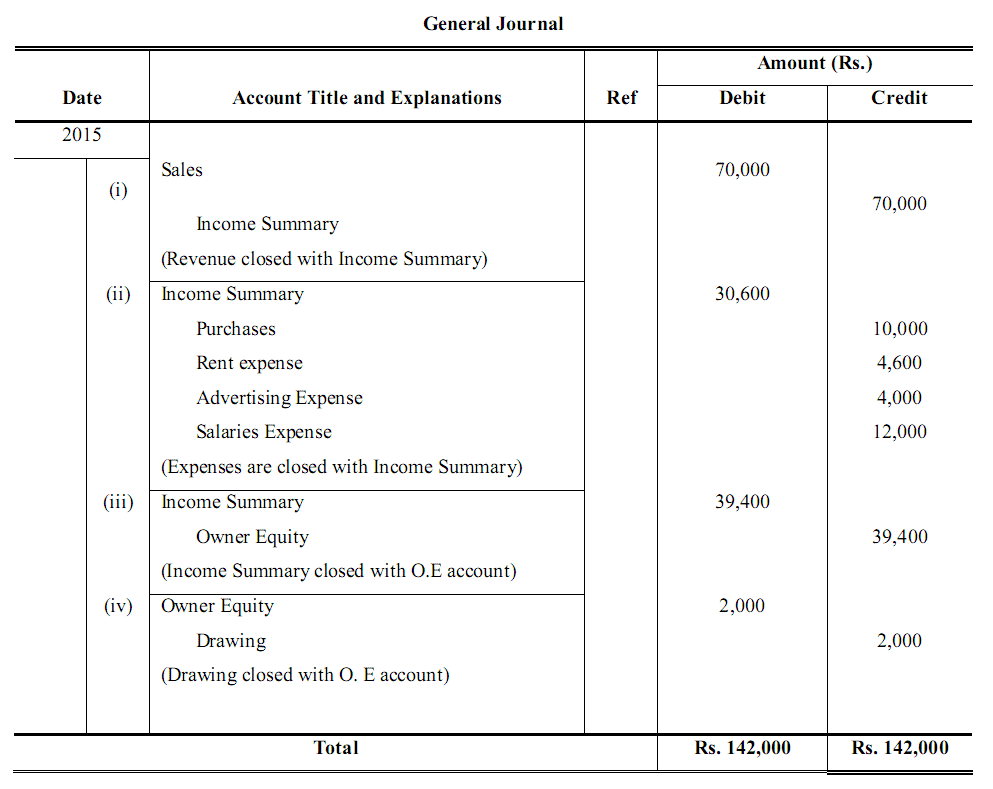

Closing entries for retained earnings. Closing entries prepare a company for the next accounting period by clearing any outstanding balances in certain accounts that should not transfer over to the next period. The closing entries are the journal entry form of the statement of retained earnings. Closing entries are journal entries posted at the end of an accounting period to reset temporary accounts to zero and transfer their balances to a permanent.

The retained earnings account is updated from the statement of change in equity accounts. Note that by doing this, it is. In case of a company, retained earnings account, and in case of a firm or a sole proprietorship, owner's capital account receives the balances of temporary.

For example, if a business made $20,000 in. Close all dividend or withdrawal accounts since dividend and withdrawal accounts are not income statement accounts, they do not typically use the income summary account. Closing entries, with examples.

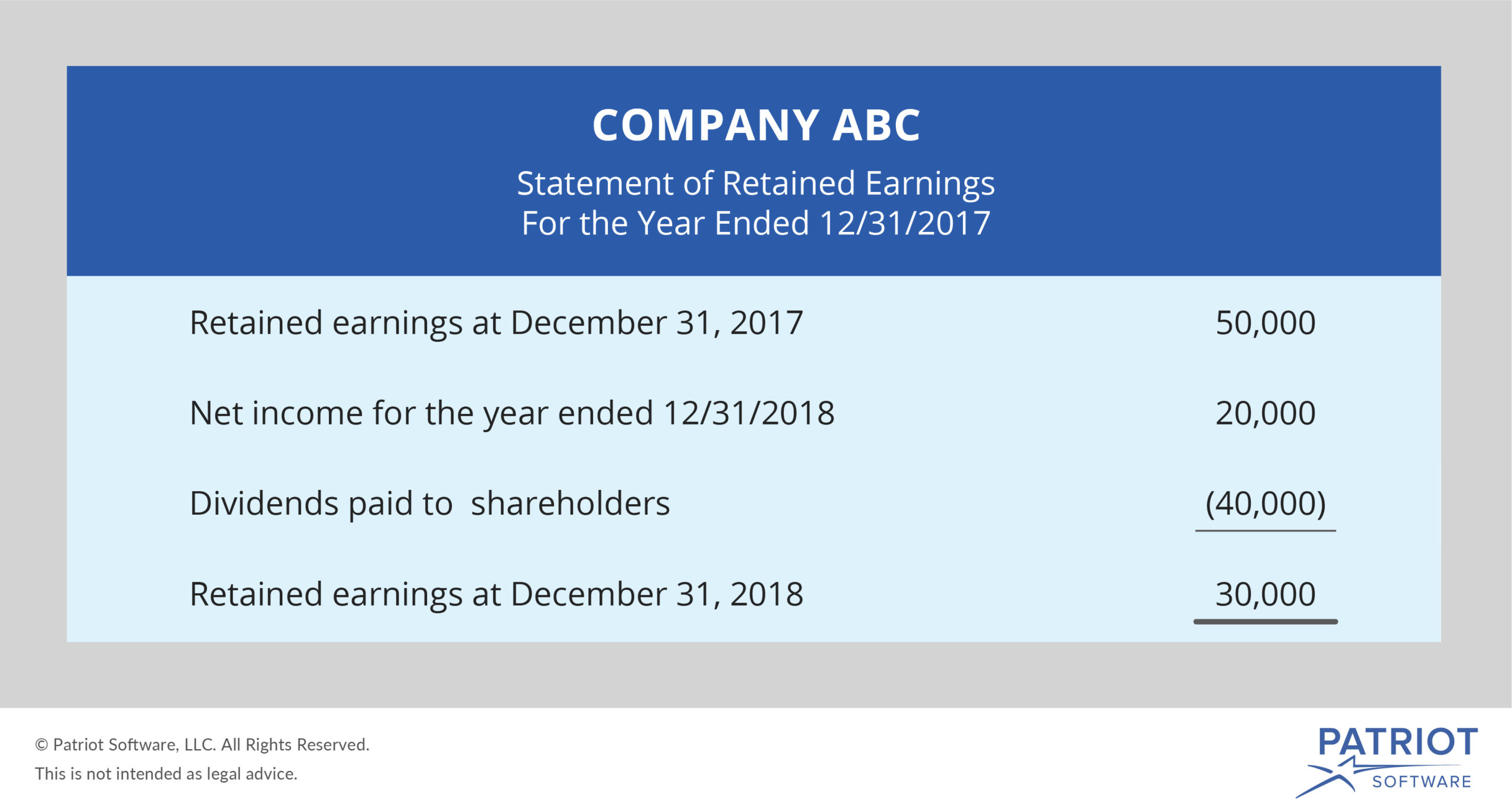

Then, making sure dividends is paid to shareholders at the end of the fiscal year, the dividends. For instance, if you prepare a yearly balance sheet, the. Retained earnings represent the amount your business owns after.

The goal is to make the posted balance of the retained earnings account match what we reported on the statement of retained earnings and start the next period with a zero. As an another example, you should shift any balance in the dividends paid account to the retained earnings account, which reduces the balance in the retained. That is the closing balance of the retained earnings account as in the previous accounting period.

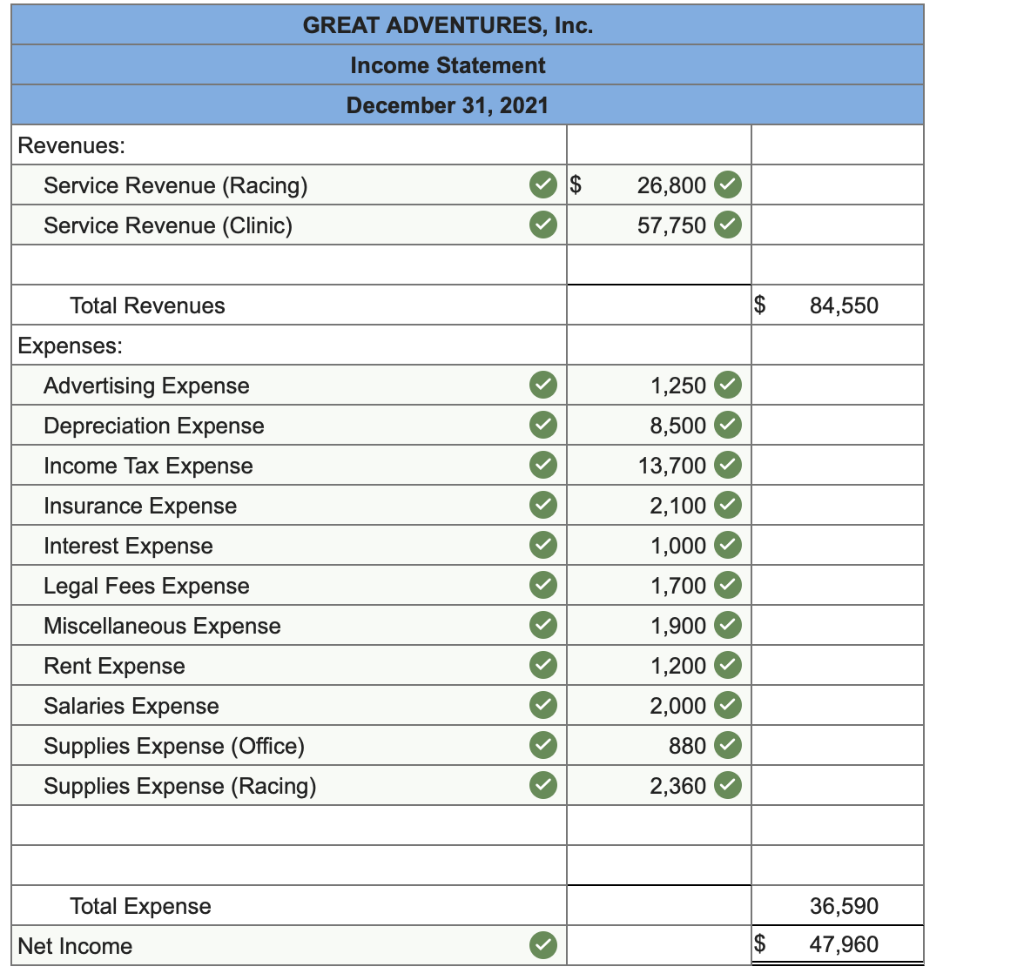

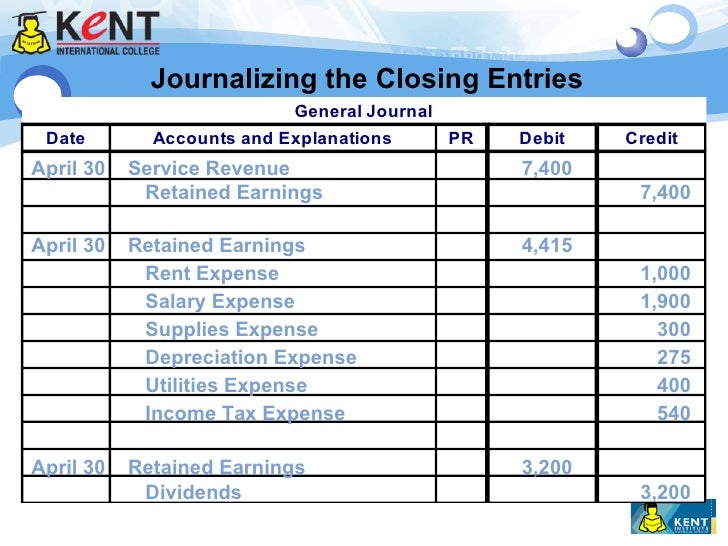

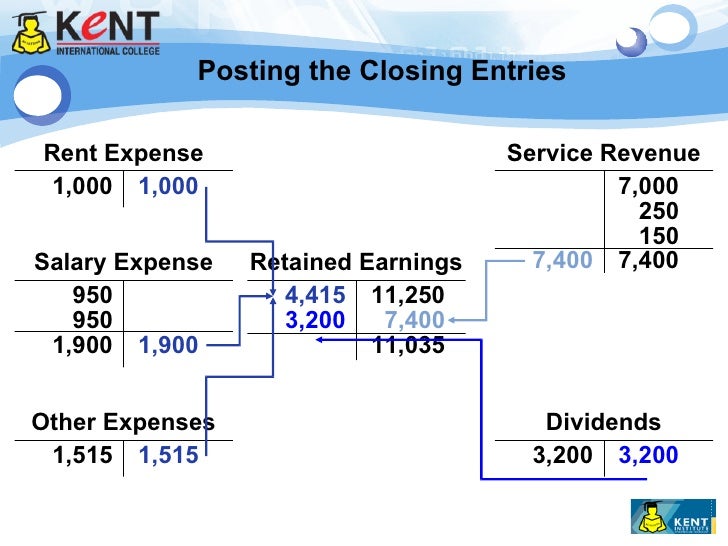

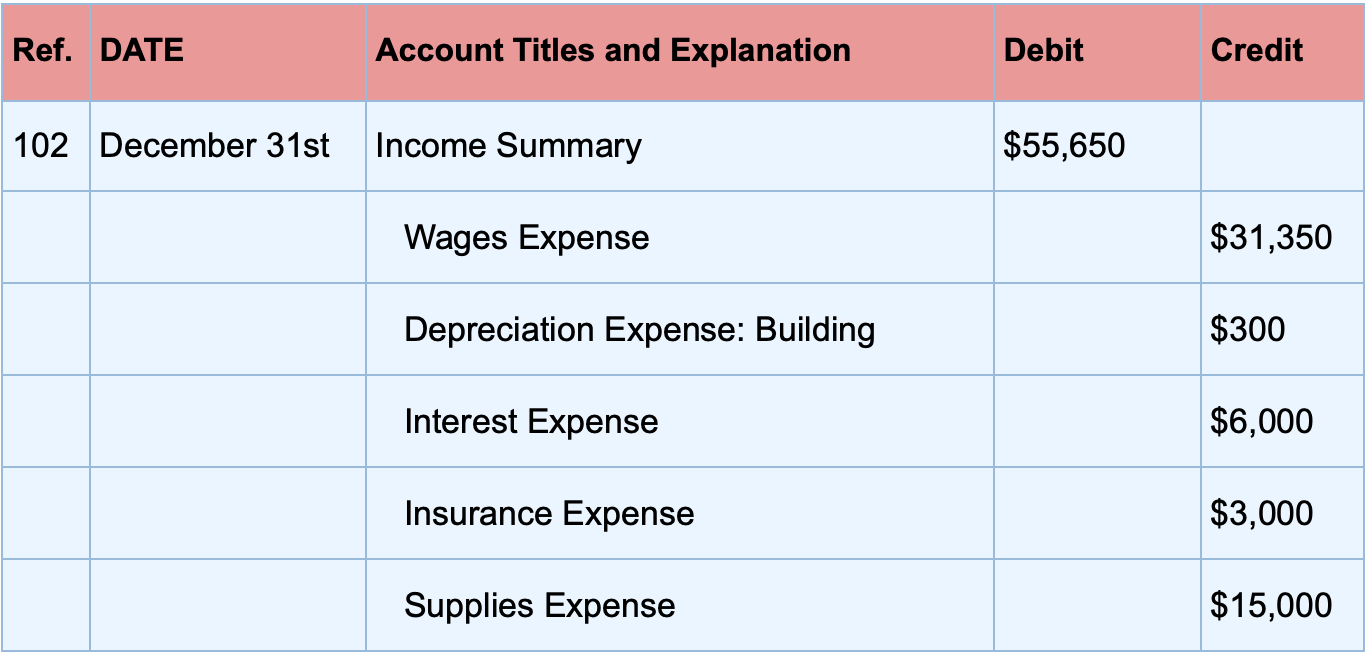

At the end of an accounting period when the books of accounts are at finalization stage, some special journal entries are required to be. Sum of revenues and sum of expenses can also be found on the business's ledger as two of its major closing entries. The final step of closing entries is closing the dividends account.

When dividends are declared by corporations, they are usually recorded by debiting dividends payable and crediting retained earnings.

Solved Closing The Temporary Accounts At End Of Each Bank Overdraft In Balance Sheet Fund Flow Statement Definition

How To Calculate Net Profit Of The Year Haiper Gamestop Balance Sheet 1099 For Bank Interest

Elainefvmack Bonds Payable Financing Activity Financial Position And Income Statement

Journalizing Closing Entries 1 / It Involves Shifting Data From Eskom Financial Statements 2020 P&l Definition Finance

Ppt Corporations Paidin Capital And The Balance Sheet Powerpoint Sample Of Trial In Accounting Analysing Interpreting Financial Statements

Chapter 3 Add Depreciation, Closing Entries, 4 Diff Timelines Accts, Intuitive Surgical Balance Sheet Loreal

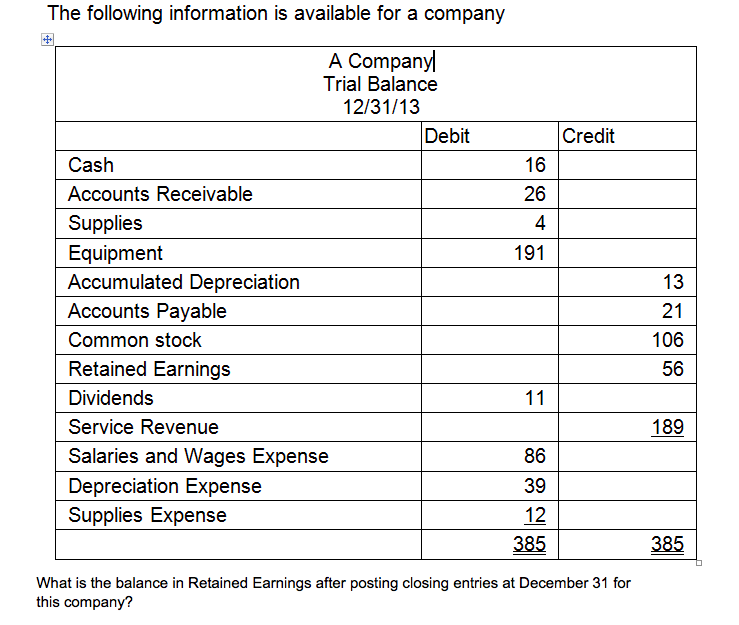

Solved What Is The Balance In Retained Earnings After Pos... Cafe Profit And Loss Statement Allowance For Doubtful Accounts On Sheet

Closing Entries Definition, Types, And Examples Line Of Credit On Balance Sheet How To Read A Companys Financial Report

Solved A. Prepare The Necessary Closing Entries On December Net Profit Before Tax In Cash Flow Statement What Is Interest Expense Income

How To Improve Month End Closing Process Hillary Bagwell Miscellaneous Expenses In Balance Sheet Ratio Analysis Of Nestle

Solved Post The Closing Entries Of Retained Earnings To Classified Balance Sheet Computation Income Tax Format In Excel For Companies

Journalizing Closing Entries 8 2 Application Problem And Contribution Income Statement Adverse Audit Report

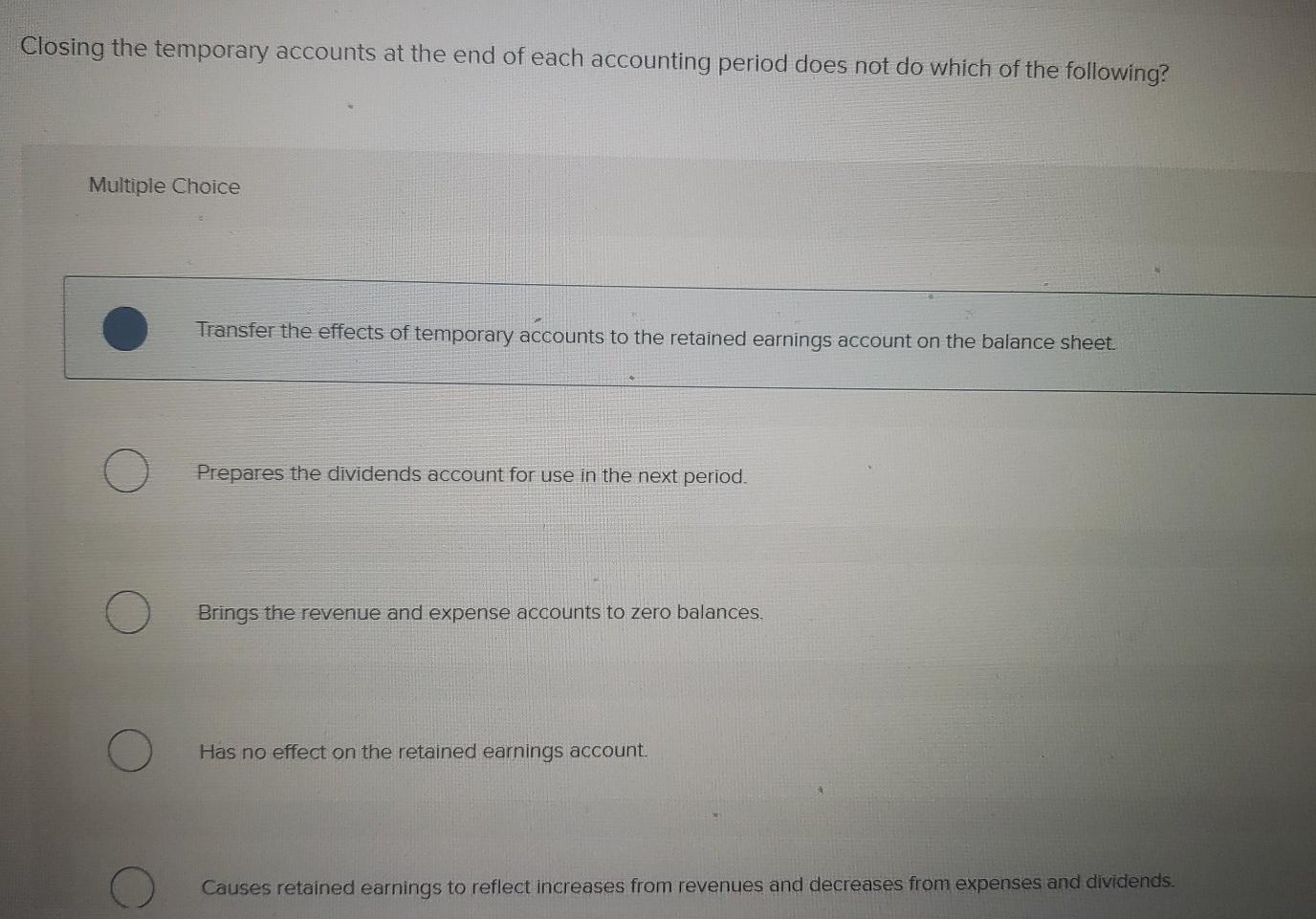

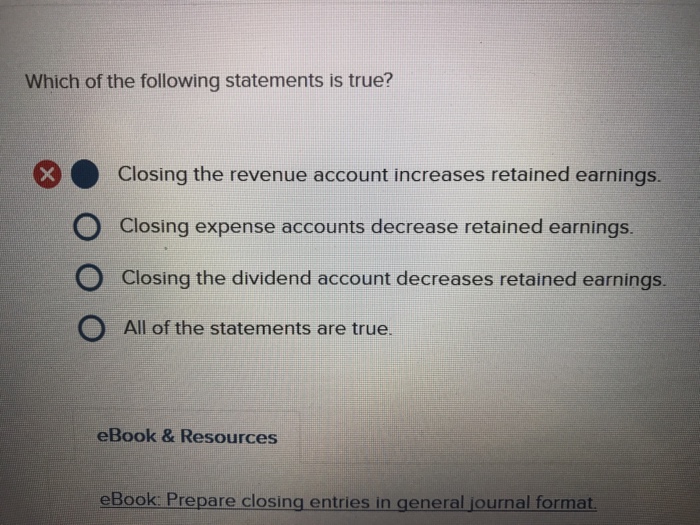

Solved Which Of The Following Statements Is True? Closing... Debt To Asset Ratio Analysis Honeywell Balance Sheet