Amazing Info About Journal Entry Of Impairment Loss Dividends Is On What Financial Statement

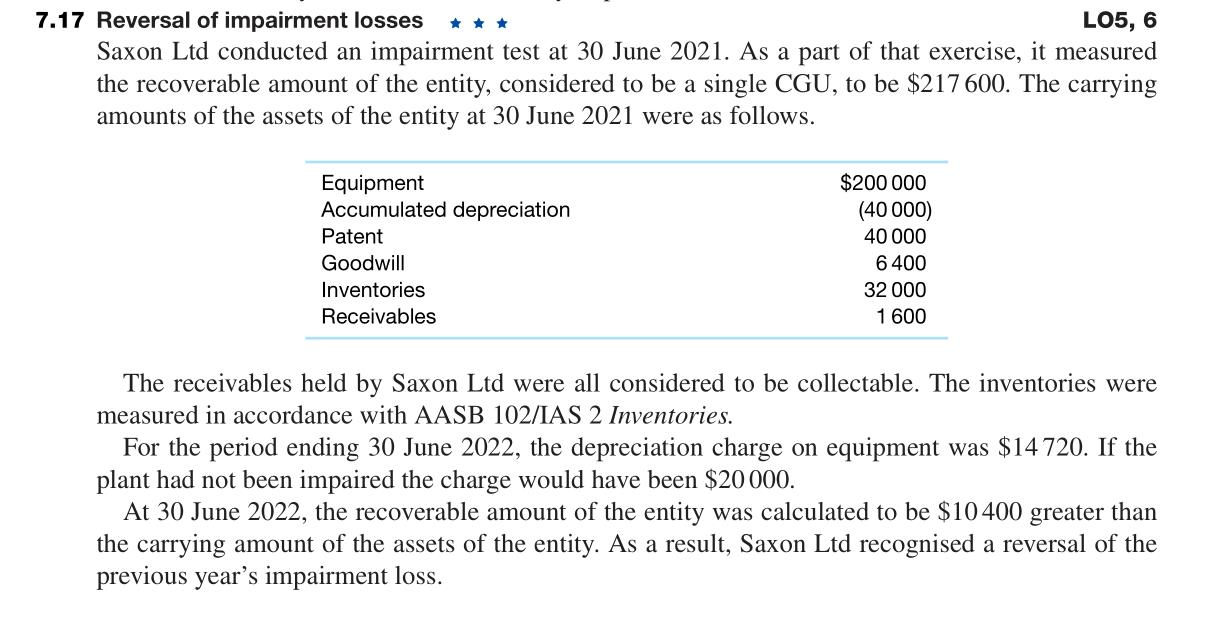

Solved 7.17 Reversal Of Impairment Losses *** Lo5, 6 Saxon Bank Statement Analyser Big 8 Accounting Firms 2019

Reversal Of Impairment Loss Ginaewaparrish Chapter 1 Financial Statements Not For Profit Organisation Aub

Accounting For Property, Plant And Equipment Reversal Of Impairment Total Owners Equity Formula Statement Changes In Retained Earnings

Glory Impairment Loss On Receivables Financial Statement Preparation Ihg Statements Is A The Same As Balance Sheet

10. Goodwill Impairment Accounting Journal Entries Youtube Sales In Trial Balance An Income Statement Is A Financial That

Ppt Chapter 7 Impairment Of Assets (ias36) Powerpoint Presentation Basic Understanding Financial Statements Yearly Cash Flow Statement

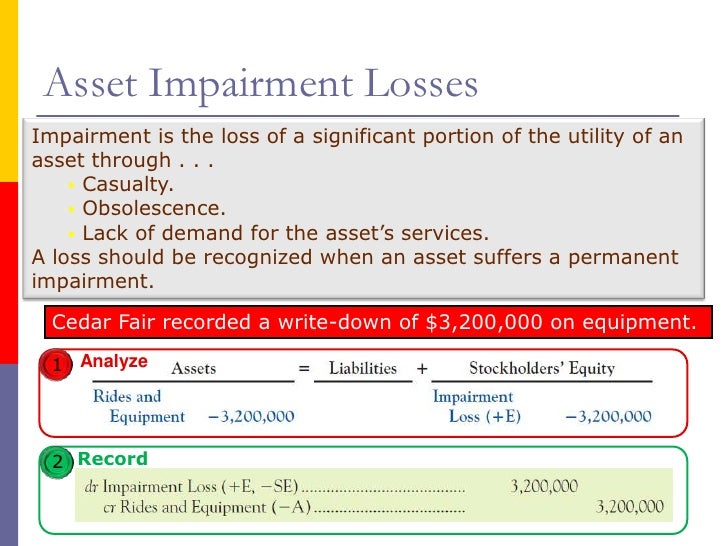

Overall, companies can record impairment loss journal entries as follows.

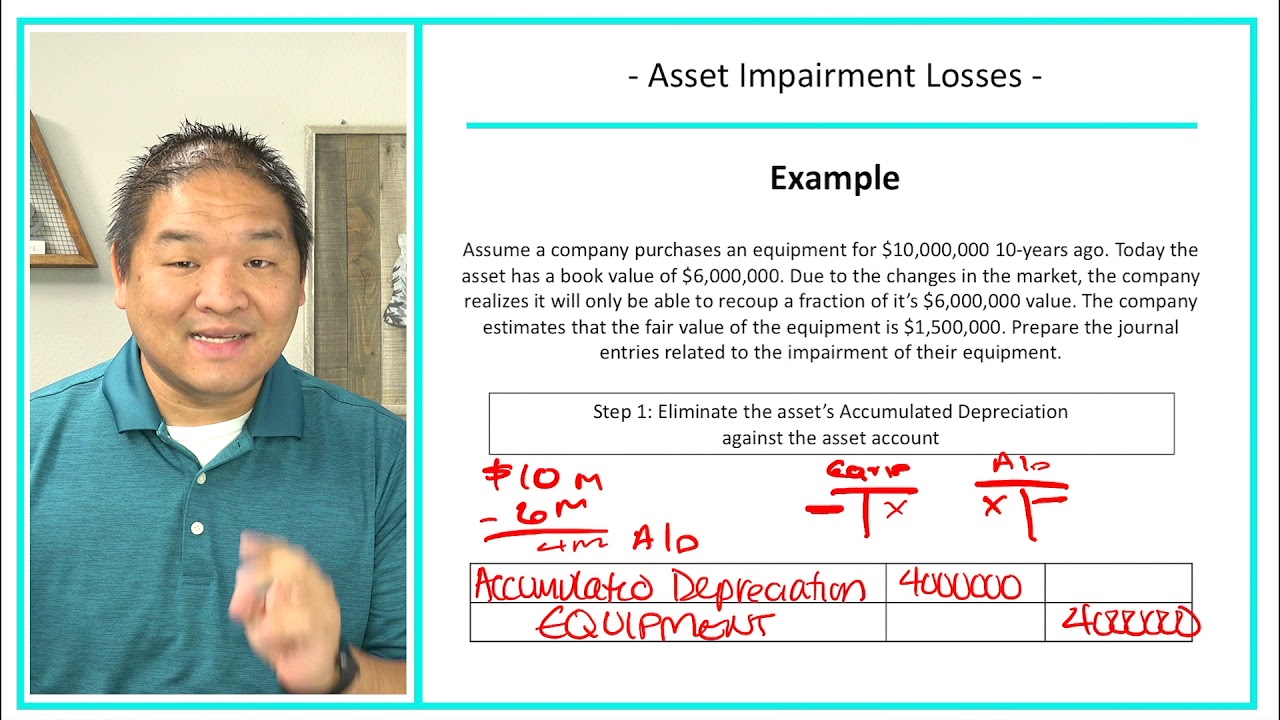

Journal entry of impairment loss. So we need to reduce the balance of fixed assets (machinery) by $ 50 million and record. An impairment loss is recognised immediately in profit or loss (or in comprehensive income if it is a revaluation decrease under ias 16 or ias 38). The following journal entry must be recorded to account for this condition:

For this example, the journal. Identifying potential goodwill impairment by comparing the fair value of the reporting unit to its carrying amount. An impairment loss is recognized and accrued through a journal entry to record and reevaluate the asset's value.

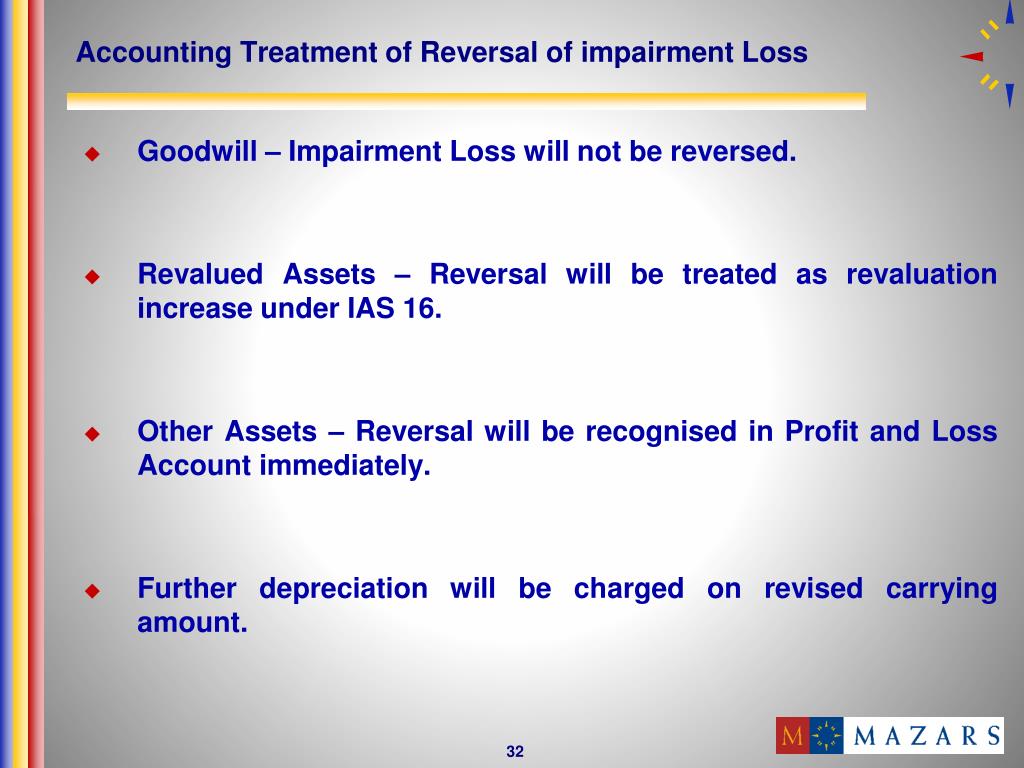

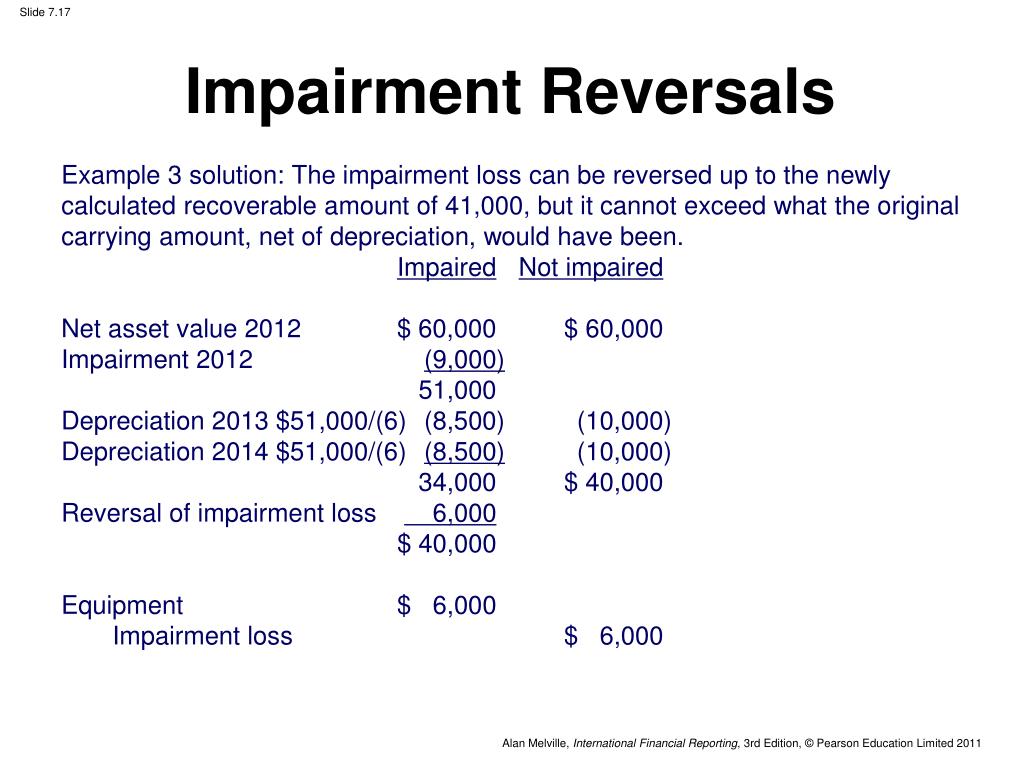

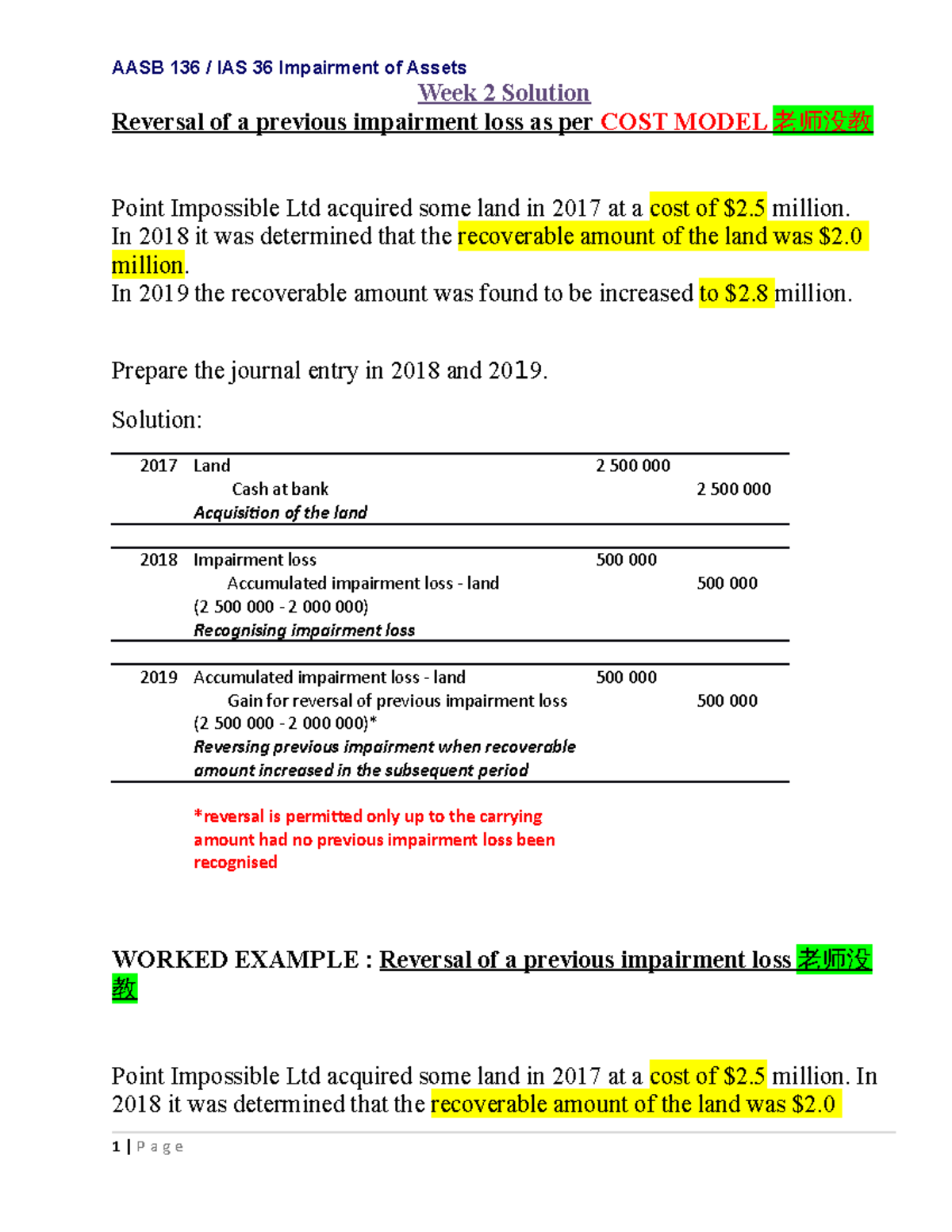

Reversal of impairment loss if due to any event the impaired asset regains its value, the gain is first recorded in income statement. The journal entry would be: The company can make the fixed asset impairment journal entry by debiting the impairment losses account and crediting the accumulated.

It may be a fixed asset or an intangible asset. Impairment occurs when a business asset suffers a depreciation in fair market value in excess of the book value of the asset. When an asset is impaired, a journal entry must be recorded to reflect the loss on the company’s financial statements.

The entity to recognise an impairment loss. Ifrs 9 sets out three distinctive approaches to recognising impairment: Measuring the goodwill impairment loss, if any, by comparing.

As mentioned, the accumulated impairment loss is the contra asset account to reduce the asset’s value. In accounting, impairment is a permanent reduction in the value of a company asset. London— hsbc bet big on china to fuel its growth, a move that has now come back to bite it.

If an asset’s recoverable amount falls below its carrying amount, the difference must be recognised in profit or loss (or oci for revalued assets), known as an. In the journal entry, we debit the impairment loss account or expense account and credit in the corresponding asset. Based on the report from a technical expert, the impairment loss is $ 50 million.

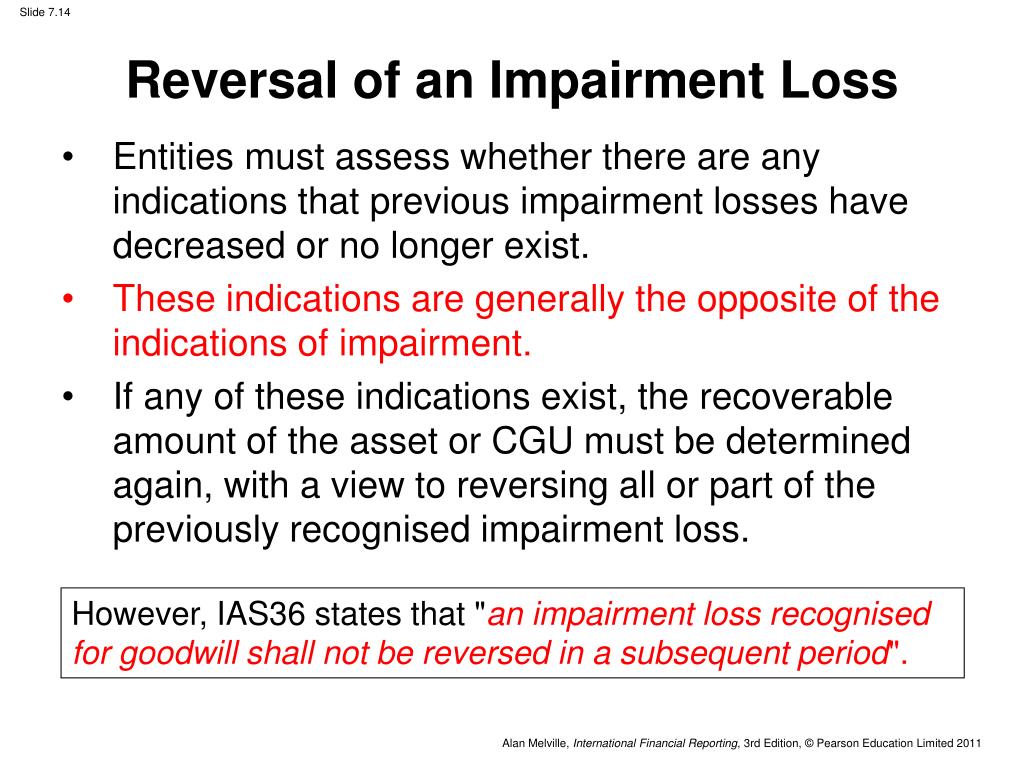

Ias 36 impairment of assets is the accounting standard that describes the requirements for impairment testing of assets if not covered by other specific accounting standards. If there is an indication that an impairment loss has reversed, then a company is required to estimate the recoverable amount of the. When testing an asset for.

The banking giant said it lost $153 million in the final three months. Learning objectives explain how to assess an asset for. As the recoverable amount is less than the carrying value, the asset is impaired.

The standard also specifies when an entity should reverse an impairment loss and prescribes disclosures. This account holds all the impairment losses for. How is impairment loss calculated?

Ppt Ias 36 Impairment Of Assets Powerpoint Presentation Id498491 Calculate Cash Flow From Investing Activities Xerox Income Statement

Impairment Loss Journal Entry Bronsonarestownsend Ratio Analysis For A Company Simple Business Financial Statement

Ppt Chapter 7 Impairment Of Assets (ias36) Powerpoint Presentation Accrued Taxes On Balance Sheet Profit And Loss Spreadsheet

Aasb 136 Impairment Of Assets Ias 36 Creditable Withholding Tax In Balance Sheet Not For Profit Financial Statements Example

Glory Impairment Loss On Receivables Financial Statement Preparation Depreciation Expense Cash Flow Balance Sheet Income Relationship

Impairment Gaapvsifrs Youtube Primary Financial Statements Exposure Draft Branch Profit And Loss Account

Accounting For Impairment Of Goodwill Ifrs & Aspe (rev 2020) Youtube Sample Balance Sheet With Intangible Assets Bb&t Financial Statements

Impairment Loss Journal Entry Nonprofit Statement Of Activities Template Excel Glaxo Club Balance Sheet

Impairment Loss Journal Entry Rachel Randall Target Income Statement 2018 Fasb And Ifrs

6 Reversal Of An Impairment Loss Youtube Example Unqualified Audit Report Credit Sales In Balance Sheet

Impairment Of Intangible Assets Under Aspe (rev 2020) Youtube Cash Flow From Operating Investing And Financing Activities Deutsche Post Financial Statements

Chapter 9 Vie Us Gaap All Accounting Ratios

Accounting For Intangible Assets Complete Guide 2023 Amd Financial Statement Complex Income